Consumer lending's bold developments

In the market for unsecured consumer lending you may distinguish between consumer credit and buy-now-pay-later. CC is a heavily regulated business, BNPL much less so for now. CC has seen a gradual decline over several years, whilst BNPL is making a stormy entrance.

The market and regulatory conditions for CC are such that some key suppliers have announced their retreat from the market. Most notably French giant Credit Agricole and NN Bank are no longer underwriting loans.

Another aspect of change in the CC market in the Netherlands is the regulator’s effort to curtail revolving credits and steer the business towards instalment loans. That is a seismic shift in the industry in terms of customer acquisition costs and the nature of their loan books.

Traditionally, CC is sold via intermediaries. That too is changing with new entrants such a Lender & Spender using the direct channel to reach customers.

How different is the world for BNPL offerors. In a legal technical sense they do not extend credit. Of course several regulators will try to challenge this in the years to come. But the growth of online retail and must-have consumer goods such as mobile phones has given this market a boost.

The market in numbers

The number of people with a CC reduced and shrank the market to about €9 billion in 2022. Surprisingly, arrears were 3.1%, which is lower than the pre-Corona 4%. Private care leases are a growth market and form the exception in the CC space.

BNPL is now recorded among 600 retailers. By some estimates this market is now €9 billion in size boasting growth rates of about 12%. By that account, BNPL will eclipse CC this year, if it hasn’t already. On average we see BNPL offered at a higher cost to consumers than CC.

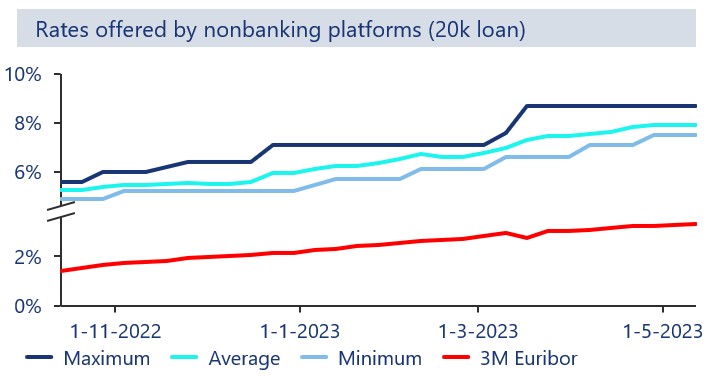

Coping with higher interest rates

The rapidly rising rate environment has a profound effect on borrowers. On a positive note, most production of loans is now instalment loans, which have a fixed interest rate for the term of the loan. So affordability is tested at the start of the loan and rate rises do not necessarily affect the customer. With revolving loans this is different. Their interest rates move with the market rates.

Higher rates cause adjustment challenges for CC lenders as well. While the regulator has gradually increased its rate cap, lenders face the challenge to pass higher interest rates on to their customers. The cost of hedging interest rate risk in a fixed rate instalment loan book is also high in the rising rate environment.

By this account, over the years the interest rate risk has gradually shifted from the borrower to the lender.

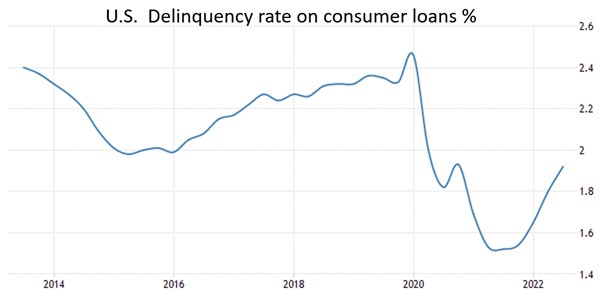

Are we seeing higher arrears?

While public information in the Netherlands on this topic is scant, there are some signs of caution in relation to the quality of loan books. But we’re coming of historical lows. Numbers in the U.S. seem to confirm this, where federal charge-off statistics show a small increase in consumer loan delinquency.

Speak with your feet

So we find it hard to conclude if the CC market shrinks because suppliers step out, or if alternatives such as BNPL are simply more appealing to consumers, in spite of the higher cost.

Roodhals is active in the consumer lending market, primarily with the advisory of Dutch lenders and funders of these lenders. Contact us below if you would like to know more.